Econometrics, version 60 (TUSUR)

Sold 0

Refunds 0

Good feedbacks 0

Bad feedbacks 0

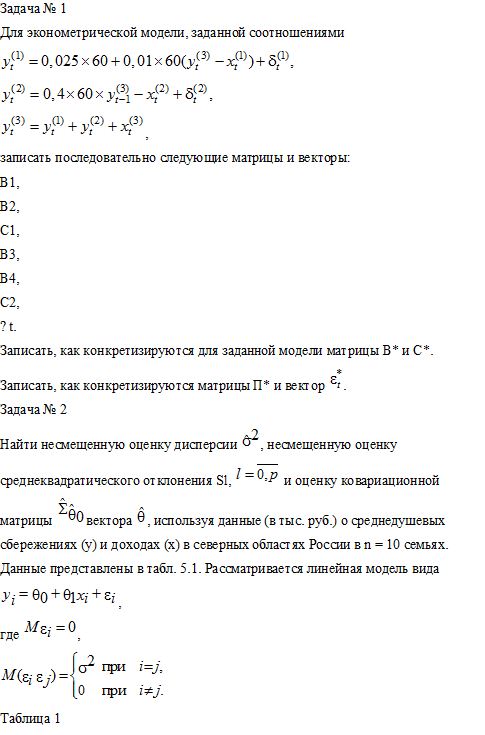

Problem number 1

For the econometric model, a predetermined ratio

record the following sequence of matrices and vectors:

B1,

B2,

C1,

B3,

B4,

C2,

Δt.

Write as are specified for a given model matrix B * and C *.

Record how are concretized matrix P * and the vector.

Problem number 2

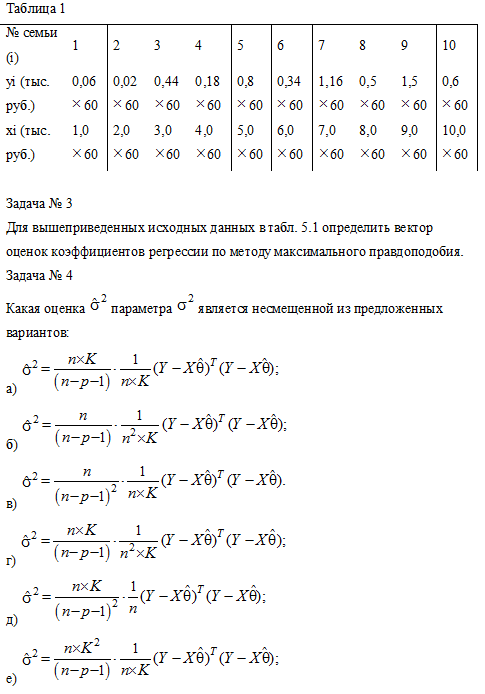

Find an unbiased estimate of variance unbiased estimate of the standard deviation of Sl, and evaluation of the covariance matrix of the vector using the data (in th. Rub.) On the average per capita savings (y) and income (x) in the northern regions of Russia n = 10 families. Data are shown in Table. 5.1. A linear model of the form

.

where

Table 1

Number of family

(I) 1 2 3 4 5 6 7 8 9 10

yi (thous. rub.) 0.06 60

60 0.02

60 0.44

60 0.18

0.8

60

60 0.34

60 1.16

0.5

60

1.5

60

0.6

60

xi (thous.

rub.) 1.0

60

2.0

60

3.0

60

4.0

60

5.0

60

6.0

60

7.0

60

8.0

60

9.0

60

10.0 60

Problem number 3

For the above initial data in Table. 5.1 determine the vector of regression coefficients by the method of maximum likelihood.

Problem number 4

What is an unbiased estimate of the parameter of the options:

a)

b)

c)

g)

d)

e)

x)

List of used literature

For the econometric model, a predetermined ratio

record the following sequence of matrices and vectors:

B1,

B2,

C1,

B3,

B4,

C2,

Δt.

Write as are specified for a given model matrix B * and C *.

Record how are concretized matrix P * and the vector.

Problem number 2

Find an unbiased estimate of variance unbiased estimate of the standard deviation of Sl, and evaluation of the covariance matrix of the vector using the data (in th. Rub.) On the average per capita savings (y) and income (x) in the northern regions of Russia n = 10 families. Data are shown in Table. 5.1. A linear model of the form

.

where

Table 1

Number of family

(I) 1 2 3 4 5 6 7 8 9 10

yi (thous. rub.) 0.06 60

60 0.02

60 0.44

60 0.18

0.8

60

60 0.34

60 1.16

0.5

60

1.5

60

0.6

60

xi (thous.

rub.) 1.0

60

2.0

60

3.0

60

4.0

60

5.0

60

6.0

60

7.0

60

8.0

60

9.0

60

10.0 60

Problem number 3

For the above initial data in Table. 5.1 determine the vector of regression coefficients by the method of maximum likelihood.

Problem number 4

What is an unbiased estimate of the parameter of the options:

a)

b)

c)

g)

d)

e)

x)

List of used literature